AMA's Insurance Program

Is it real? Is it adequately funded? How much of AMA dues is involved? Where is the money to back it up? — John Worth

Part I — The Commitment

Last year, AMA's Executive Council (equivalent to a corporation's Board of Directors), faced with having received no offers from the insurance industry to provide continuing coverage for AMA members, clubs, and flying site owners, after an exhaustive search, made a bold commitment to provide the protection that has been the backbone of AMA membership for many years: the Council approved AMA's funding of its own liability protection program.

The Council decided that AMA would put up the money to finance the program. However, because AMA is not permitted to sell insurance, it was necessary to do this through a commercial insurance company. AMA, therefore, contracted with such a company, United National of Philadelphia, to provide (for a fee) a policy and the services related to it.

Multi-Level Funding

AMA provided the company with a basic fund of $218,350 for claim coverage and backed it up with a bank Letter of Credit in the amount of $806,650, to cover any claims beyond the basic fund. This arrangement made available slightly over one million dollars of coverage.

Further, to help assure that this amount would not be wiped out or reduced by one or more claims, it was approved that an additional half-million dollars would be set aside by AMA up front to cover claim actions before calling on the funds under insurance company control.

In other words, to "guarantee" the availability of one million dollars of coverage, a half-million was put ahead of it; a sort of half-million dollar "deductible" to be paid by AMA before the insurance company would have to make any payments.

To handle the "up front" half-million, a separate contract—also for a fee—was made with Alexsis (of Alexander & Alexander of Omaha) to service claims and to handle all reporting of them to AMA. Meanwhile, the "up front" half-million was put into a separate account from all other AMA funds (actually into an interest-bearing Money Market Fund of the First American Bank of Virginia—incidentally, that account had already earned over $11,000 interest by the end of May 1987, averaging about $2,000 per month since being established late last year).

In this manner a million and a half dollars of liability protection is provided. In addition, as of April 25, 1987, the Executive Council added even more money to the program. To maximize the opportunity for the half-million to earn interest, the Council established an Insurance Operating Buffer of $120,000, to be used ahead of the half-million for routine and relatively minor claims.

Thus, the "up front" half-million protects the one million controlled by the insurance company, and the $120,000 buffer protects the half-million. This multi-layered approach is both appropriate and prudent since it helps to assure that we don't nibble away at the major amounts during routine daily business. It makes it easy to see and to show, to anyone who requires proof, that the major amounts adding up to one and a half million, minimum, are not touched except in a severe claim situation.

AMA's Claim Record

Past experience under former insurance policies indicates that this three-tiered program should be adequate.

A 10-year study of AMA's previous insurance programs showed that we averaged about $70,000 annually in claims costs (separate from insurance premiums paid to provide the coverage). Thus, if this experience continues, the $120,000 per year operating fund should cover "normal" annual claims—the claims situation would have to be unusual to require going beyond the operating fund and the million-and-a-half coverage.

Is a million-and-a-half coverage enough? Based on the past 10 years (actually 45 years—AMA has been providing coverage since 1942) it should be more than enough. But there can be an exceptional claim situation at any time, so there needs to be a reserve much larger than what past history showed was enough. For now, it appears that a million and a half is adequate to back up our one million dollars of advertised coverage.

Reserves

Claims are often made long after an accident. Thus, for any claim situation, reserves need to be set aside to cover eventual settlement. This means that reserves must be allocated each year for potential claims from accidents in that year. This in turn means that reserves must be continually added to, year by year, to assure that we are not depending only upon the current year's funds. For example, AMA currently has over $300,000 in reserve for prior year's claims, completely separate from the funding for the current program.

In this situation it might seem that there could never be enough money available for potential claims. Experience suggests otherwise, as reality is usually kinder than possibility—that's what the whole insurance industry is based on: the "laws" of probability.

In general, assuming that we got by our first year in the new program without exhausting our reserves, we should be able to build and improve our insurance funding, year by year. How much is enough? "Experts" in the field have indicated that three million in reserve will probably be adequate; five million for sure.

This means a long-range commitment to the program is necessary. We are not going to be able to fund a three- to five-million reserve program in one year. Based on the current AMA dues structure, the higher level of funding should be possible within a few years, possibly as early as 1990.

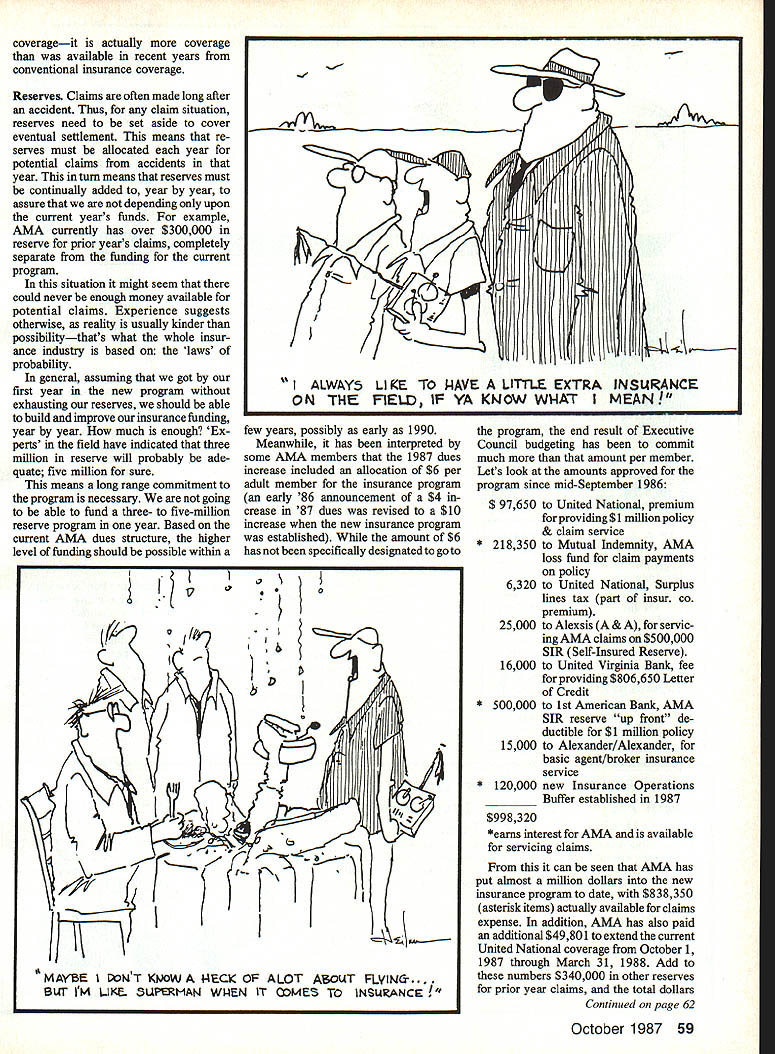

Meanwhile, it has been interpreted by some AMA members that the 1987 dues increase included an allocation of $6 per adult member for the insurance program (an early '86 announcement of a $4 increase in '87 dues was revised to a $10 increase when the new insurance program was established). While the amount of $6 has not been specifically designated to go to the program, the end result of Executive Council budgeting has been to commit much more than that amount per member. Let's look at the amounts approved for the program since mid-September 1986:

- $97,650 to United National, premium for providing $1 million policy & claim service

- $218,350 to Mutual Indemnity, AMA loss fund for claim payments on policy

- $6,320 to United National, surplus lines tax (part of insurance company premium)

- $25,000 to Alexsis (Alexander & Alexander), for servicing AMA claims on $500,000 SIR (Self-Insured Reserve)

- $16,000 to United Virginia Bank, fee for providing $806,650 Letter of Credit

- $500,000 to First American Bank, AMA SIR reserve "up front" deductible for $1 million policy (earns interest for AMA and is available for servicing claims)

- $15,000 to Alexander & Alexander, for basic agent/broker insurance service

- $120,000 new Insurance Operations Buffer established in 1987

Total: $998,320

From this it can be seen that AMA has put almost a million dollars into the new insurance program to date, with $838,350 (the asterisk items above) actually available for claims expense. In addition, AMA has also paid an additional $49,801 to extend the current United National coverage from October 1, 1987 through March 31, 1988. Add to these numbers $340,000 in other reserves for prior year claims, and the total dollars available for claims and reserves exceeded $1,388,000.

At the time, many insurance companies were changing the way they wrote coverage. For example, companies would no longer offer the open-ended, per-occurrence limit.

Instead of saying that up to one million dollars of coverage was available per accident (occurrence), with the potential of a number of accidents and multiple millions of dollars of coverage, the insurance industry tightened up and began limiting the total number of dollars to be paid out under any one policy, using the term "aggregate" to describe the difference.

The difference wasn't appreciated at first because past experience indicated that no problem should result. This was based on the fact that one million dollars had been more than enough to cover any one year's total claims.

Thus AMA accepted the transition in terminology without making a point of it; first, because we had no choice (it was a take-it-or-leave-it situation) and second, no real effect on coverage was expected. More recently, however, the nature of claims settlements has changed, with substantial increases an apparent trend. With this situation grew concerns about how much total coverage would be enough.

What developed was a perception that where a million dollars of coverage was enough previously, on a per-occurrence basis, it might not be enough for an aggregate situation. In other words, where past experience had shown that in any one year one million dollars could provide more than enough coverage for multiple claims, more recent experience suggested that the potential for more claims of higher dollar value could change the picture.

Thus, the aggregate limit was imposed to put a ceiling on possible claim pay-outs, so that insurance companies would know exactly how much financial exposure they would be at risk to cover. Regardless, for modeling activity, the difference appeared to be only in terminology. Claim experience stayed well within the million-dollar umbrella.

But in an atmosphere of controversy that developed in recent years, between the insurance and legal industries, over amounts of coverage and sizes of settlements, some people began to focus on the word "aggregate," and fears were expressed that a one-million-dollar aggregate might no longer be enough to cover modeling activity.

Meanwhile insurance coverage became harder to get. Even where coverage could be obtained, the price went up drastically. It finally reached the point where so much was being spent for insurance premiums, rather than claims, that AMA seriously began to consider funding its own insurance program. When commercial insurance finally became impossible to buy, at any price, even companies with very favorable low-claim experience, AMA went on its own.

However, because AMA cannot legally be in the insurance business, it was necessary to work through a commercial company to provide an insurance policy. This meant accepting the current insurance terminology, based on the fact that AMA's resources were limited, so that an aggregate limit was necessary, since there are no insurance industry reserves to come into play if AMA's funding fell short.

AMA, therefore, has a policy using the word "aggregate." Past experience says that it shouldn't matter since we don't expect to reach that limit. Still, to help reassure anyone concerned that AMA has enough funding for the protection that people (members, clubs and flying site owners) have come to expect, AMA put another half-million dollars of coverage ahead of the one million dollars of coverage available through the insurance policy. And AMA has gone even further by putting still more money up front — another $120,000 ahead of the half-million!

Thus, the "real" aggregate protection against claims is more than a million and a half dollars, regardless of what the insurance policy says. AMA's commitment, therefore, goes beyond the insurance company policy, with a three-tiered program designed to protect the total modeler activity, including members, clubs and flying site owners. Furthermore, AMA continues to seek, at realistic cost, additional insurance to protect against any catastrophic-type situations.

To sum up, the aggregate policy serves to assure that claims will not exceed AMA's funds. Yet those funds should be adequate, based on many years of model aircraft claims experience, to assure that protection will be available if needed. With the buffers AMA has built into its protection program, any change of situation which might severely reduce funding should be preceded by ample warning so that action can be taken to solve the problem. In any case, AMA's commitment is to continue providing liability protection as it has for more than 40 years, with or without the insurance industry.

Part III — Overview

Looking back a bit may help to put the current program in perspective. Up until a few years ago (from early 1976 through late 1982) AMA paid a relatively low annual premium to buy liability insurance, averaging a little over $100,000 per year. Then the cost began to climb (despite a favorable claim rate) to about $160,000 a year between 1983 and 1985, going to $237,000 for the '85–'86 period.

During the latter years AMA began paying claims out of its own funds while continuing to buy commercial insurance, in a "deductible" type arrangement, to avoid paying even higher premiums. As a result the insurance companies did not have to pay out a single dollar for claims during the last four years! Regardless, we were not able to get an insurance company to provide a quotation for '86–'87 coverage.

Under AMA's current program we have had to commit more total funds, but the actual amount paid out to others for related services has returned to the $160,000 level. Meanwhile, the rest of the funding belongs to AMA and is earning interest. Thus, barring a calamity, our liability protection costs have stabilized. They are now under our own control (except for what claims experience may bring) rather than at the mercy and whims of the insurance industry. Now, after almost a year of the new program, the outlook is bright and the prospects good for further program improvements in 1988.

Transcribed from original scans by AI. Minor OCR errors may remain.